July 22, 2022

Last week the CRTC quietly released a disquieting study it commissioned on the decline in Canadian television broadcasters’ opportunity to buy and re-sell popular US programming on their networks.

The take-away from the report written by industry analyst Peter Miller is that the entry of more foreign, mostly American, “Direct to Consumer” (DTC) television apps into the Canadian market threatens to cancel the Canadian broadcasting system’s meal ticket.

The DTCs include the California-based studios Disney, Paramount (CBS) and Apple TV, increasingly selling exclusive access to their premium movies and hit drama series. Competing apps from Peacock (NBC) and Warner/Discovery’s HBO are potential market entrants in Canada. The DTCs compete for subscribers against Netflix and Amazon Prime but also against traditional broadcasters whose audiences watch drama and comedy shows for forty per cent of their monthly viewing hours according to the CRTC.

The popularity of US dramas with Canadian audiences drives broadcaster profits that set-off losses they sustain making Canadian news, information, sports and Canadian “programs of national interest.”

If the supply of US programming to Canadian broadcasters is severely diminished, says Miller, the rate of cable-cutting and cable-nevering will increase. That will push Bell, Corus, Québecor, and Rogers ever closer to the dreaded tipping point where subscribers and national advertisers no longer view cable TV as a must-see or a must-buy platform. Miller doesn’t make the comparison, but this is what happened in the newspaper market several years ago.

The Report says that whatever television services are most exposed to the loss of US drama programming are at the greatest risk: specialty television channels and Video-on-Demand services will suffer the most. Given that specialty TV has been the profit-engine of Canadian TV for decades (and “conventional” local stations are generally unprofitable), the Report concludes the Canadian broadcasting system faces an existential moment in the near future. Miller maps out a range of outcomes from best to worst case scenarios.

Although traditional television revenues have fallen steadily since 2014, so far the profit margins of our major media companies are holding, at least in cable distribution and specialty programming if not conventional broadcasting.

Also there is as yet no hard data measuring the loss of US programming rights: most of the CRTC’s relevant data metrics are confined to Canadian programming and Numeris does not appear to have access to data that would support a metric on the loss of US programming.

Of necessity, Miller’s observations are documented by numbers that show the revenue growth of foreign Internet TV apps in the Canadian market; the market entry of new DTC apps based on exclusive programming offerings; and a series of confidential interviews he conducted with Canadian TV executives about the declining availability of programming rights.

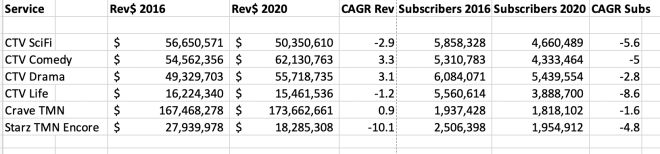

We can engage in limited data snapshots of the specialty channels most likely to be impacted by the loss of programming rights to premium American movies and drama series. As of August 31 2020, data submitted to the CRTC by our largest broadcaster Bell Media reveals revenue, subscriber and growth metrics for its key English Canadian specialty and VOD services:

As you can see revenue is treading water but subscriber numbers are falling and that can’t last indefinitely. Fresh CRTC data for 2020-2021 is due soon.

This 2020 data may or may not measure the full impact of market entry (and exclusivity practices) by Disney Plus in November 2019 and Paramount Plus (formerly CBS All Access) in 2018. At this point in time the precise pace and impact of the loss of US programming rights is still informed guess work.

A significant variable in that guess work is the entrepreneurial response by Canadian broadcasters. (An insightful article by OutTV CEO Brad Danks both acknowledges the omnipotence of the American streaming apps and suggests an entrepreneurial response).

The latest development in television business models is the emergence of free-advertising supported TV (FAST), embedded advertising for shows streaming on Internet TV platforms.

FAST could be the coup de grâce to ad-supported conventional television (already having lost market share to Google and Facebook) or it could be an opportunity to reclaim it.

Another innovation is Corus distributing its conventional programming, including Global News, on digital platforms like Fubo TV, Paramount’s Pluto TV, Amazon Prime and Roku for a negotiated fee, something not available to them from cable companies who are permitted by Canadian copyright law to retransmit broadcaster programming for free from their over-the-air signals.

Bell Media clearly would like to partner up with Netflix to make Canadian content: it unsuccessfully urged the federal government to amend Bill C-11 in a manner which would have given the CRTC the regulatory power to create co-production opportunities.

Niche Canadian programmers like OutTV, Blue Ant, and independent YouTubers are increasingly seeking out global distribution by major digital distribution platforms, a strategy available to other Canadian broadcasters.

Whether these are winning entrepreneurial plays or just whistling past the graveyard is something we will watch unfold in the next few years.

Miller’s Report recommends a government policy response, and quickly, given his projection of a major downturn in the financial viability of Canadian broadcasters impacted by the loss of programming rights. Regrettably neither the CRTC’s 2018 forecast (“Harnessing Change”) nor the 2020 report of the Broadcasting and Telecommunications Legislative Review tackled the programming rights issue or recommended any policy response.

Bill C-11 is not that policy response, says Miller.

Bill C-11 will result in an injection of $1 billion (according to government estimates) into the production of Canadian programming by foreign owned Internet TV companies. While the legislation should bring the foreign streamers’ regulatory costs up to the same level of Canadian broadcasters, it does not provide any incentives or requirements to continue selling programming rights to Canadian broadcasters instead of pushing their TV apps as the exclusive access to their hit programming.

Miller writes enigmatically at the conclusion of his report that Canada should consider a range of pro-Canadian policy measures that revive wholesaling programming rights as the most attractive option to American media companies seeking Canadian audiences:

… structural measures that financially advantage or give priority to Canadian owned and controlled broadcasting services (such as Internet advertising tax deductibility, zero rating of wireless data usage, preferential access to Canadian production financing and expanded rights protection measures) should be under serious consideration.

5 thoughts on “CRTC Report says the loss of US programming imperils Canadian broadcasters”